big xyt is a proud sponsor of TradeTech Europe 2022 on 11-12 May. Don’t miss Mark Montgomery’s panel alongside Vanguard Asset Management, Norges Bank Investment Management and Capital Group to learn about the advancements in enhanced execution analytics.

Trading turnover in European equities posted a new MiFID II era record in Q1, 34% higher than the four year average, as investors reacted to the cocktail of inflationary fears and war. Back in Q1 2020 it felt like we were watching a truly exceptional event but despite lower volatility, the markets managed to deliver something even more unpredictable. Please have a read of our latest European market microstructure and let us know your thoughts or ideas for any further investigations.

The amount of data produced globally continues to grow exponentially. Units such as Tera and Peta are no longer capturing the magnitude. As new terms such as Wispabytes and Crunchiebytes have been necessary, there are fears that the extent of this uncontrolled data production could soon have unintended consequences. Uncleansed data is not being disposed of, capacity levels are already being reached with clouds becoming saturated, and the inevitable precipitation could have irreversible effects. The Journal of Knowledge & Environmental Science (J.O.K.E.S.) has forecast that by 2030 there could be a film of excess data covering the whole of the earth’s surface.

Do you remember the optimism of the Santa Claus rally? Only a few months ago we were being entertained by stories of the S&P 500 in the high fives by year end (that would be a 30%+ rally from here) and post pandemic recoveries across the board. Then along comes the spectre of war, sanctions, and a cost of living crunch for households.

Dark trading currently represents 8% of equity turnover across all of Europe, adjusted to exclude clearly non-addressable OTC and SI prints. In UK Blue Chips that is now 11.6%, and for UK mid caps it is 15.2% How often are you looking to identify when a stock has an unexpected surge in turnover? And how often is it beneficial to know that some or all of that increase was on a Dark venue?

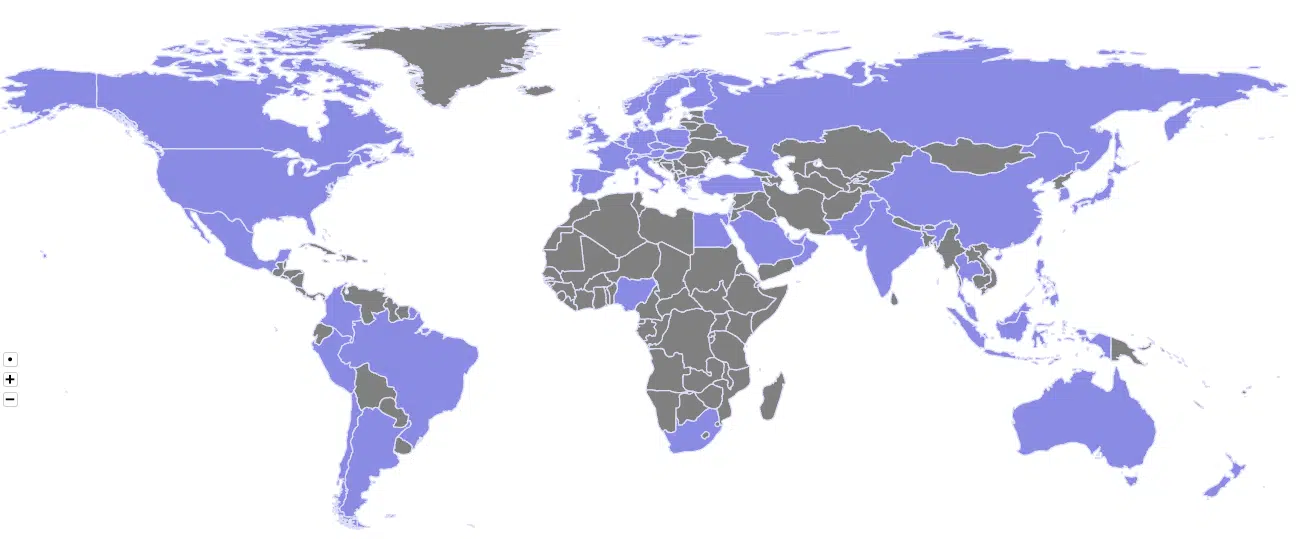

big xyt, the independent provider of smart data and analytics solutions to the global trading and investment community, today announced the launch of the Global Exchanges Directory, an interactive web portal providing key information on 97 worldwide stock exchanges and alternative trading venues in seven regional categories.

2021 has ended and all that remains are the tea leaves at the bottom of the cup. In our latest annual survey of market volumes and fragmentation trends in European equities, we gaze at the patterns to see how the story unfolded and what we can learn about the year ahead. Another turbulent year for equities globally played out in the daily ebb and flow of over 250 billion quotes, orders and trades, presented to you here in a short pictorial summary.

When Santa visited us for one of our academy sessions, Market Structure for North Pole Inhabitants, we provided an initial introduction to European market structure using the following chart for European Equities by trading mechanism, which may be familiar to many of you: Santa soon understood that, but as a wise man, he remained curious – one of the questions he asked was about ETFs: “If these equity-like instruments are called Exchange Traded Funds,” he asked with a glimmer in his eye, “Why do they trade less than 28% of their volume on exchange compared to 53% for vanilla equities?”

Santa may need to consider moving with the times as we navigate the growing wave of social responsibility. On the one hand, reindeer power is about as green as you can get to power a vehicle, and on the other…..all that wrapping paper and packaging! Someone needs to tell him ESG does not stand for Extra Special Gift. One of the recent benefits of the growth of ESG campaigns in financial markets is that the spotlight has moved beyond a focus on the social DNA of companies to invest in. Questions are now being asked about how all the companies who are active in financial markets are behaving. Could there be ways to introduce new practises and infrastructure in order to become more sustainable as an organisation, and as a community?

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Santa may need to consider moving with the times as we navigate the growing wave of social responsibility. On the one hand, reindeer power is about as green as you can get to power a vehicle, and on the other…..all that wrapping paper and packaging! Someone needs to tell him ESG does not stand for Extra Special Gift.

{kind=link}