Is the fun about to come to an end for those trying to optimise (and capitalise on) their interaction with one of the most heavily traded equities in Europe?

It has to be one of our favourite stocks for the complexity it presents for equity exposure to a single organisation. Two different lines of stock, both traded heavily on two primary exchanges. Competition aplenty from the UK and European MTFs and the full spectrum of market mechanisms accessible to trade; lit, dark, auctions, off-book (on-exchange), OTC….the list goes on. It presents a challenge for many investors, banks and brokers and a long standing opportunity for the canny arbitrageur.

We love Royal Dutch Shell for the opportunity to look at the impact of Brexit on volumes, market share, spreads, depth and so much more.

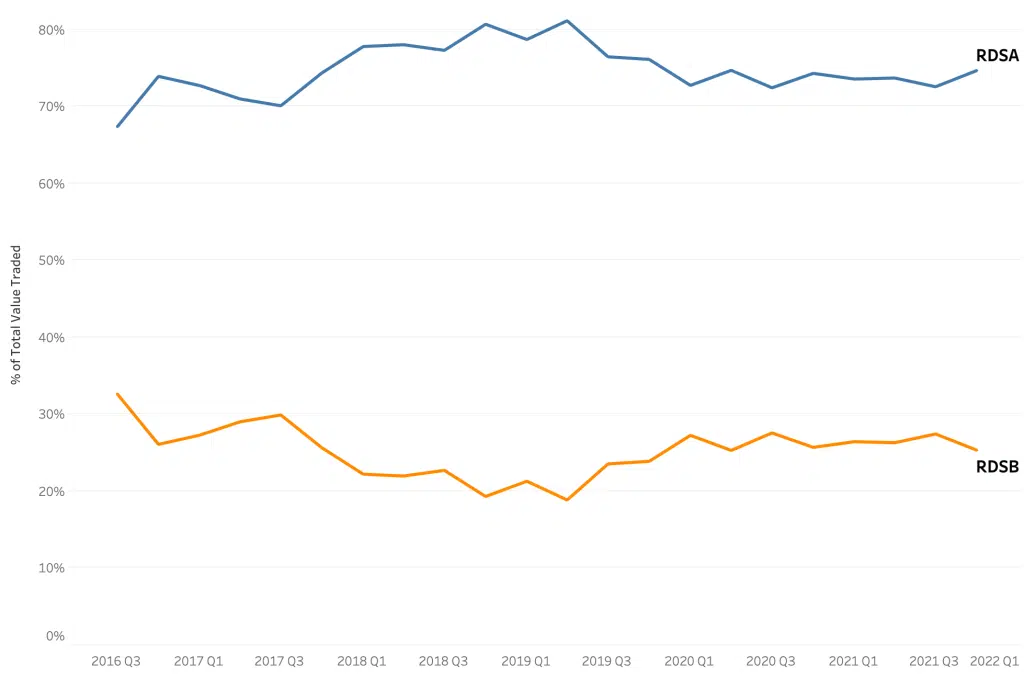

As an example, here’s how the turnover of the two lines of RDS compare over time.

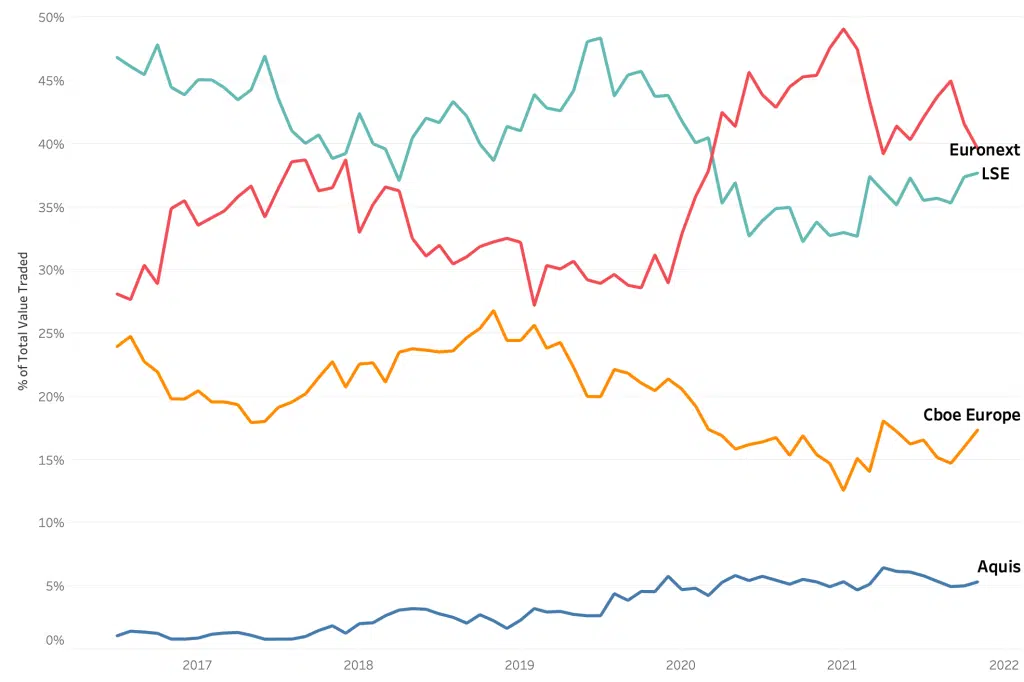

This is what the lit value traded market share looks like for the combined RDS stocks across the most active exchange groups since the end of 2016. Note the interesting shift in the primary exchange groups ranking from around the beginning of 2020.

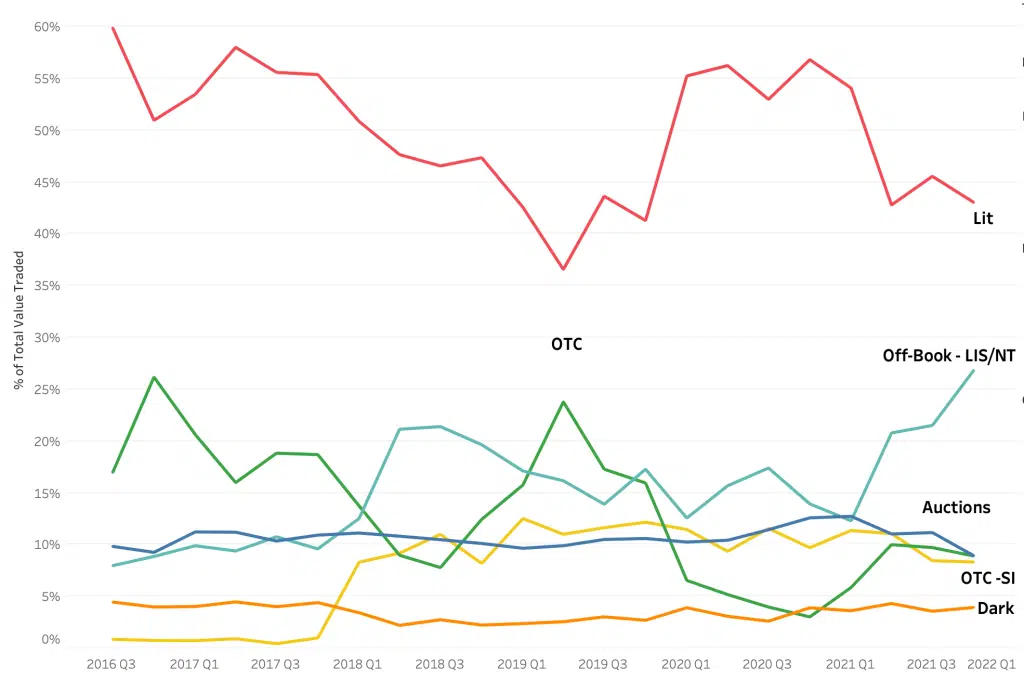

If we look at that a little more closely we see a different story emerging. The trading mechanisms used were changing at the same time; whether it was influenced by Brexit or other factors we can see below that Off-Book (On-Exchange) trading grew dramatically in that same recent period, at the expense of lit order book activity:

If the proposed simplification is approved by shareholders on 10th December and goes ahead, the removal of “Royal Dutch” may well leave an empty Shell but there is no doubt that the complexities and fragmentation of the market will mean there will still be plenty to analyse in order to access liquidity at the right price.

As a side note, the Dutch economic affairs and climate minister involved in this debate is called Stef Blok. A great name for a career on the trading floor.