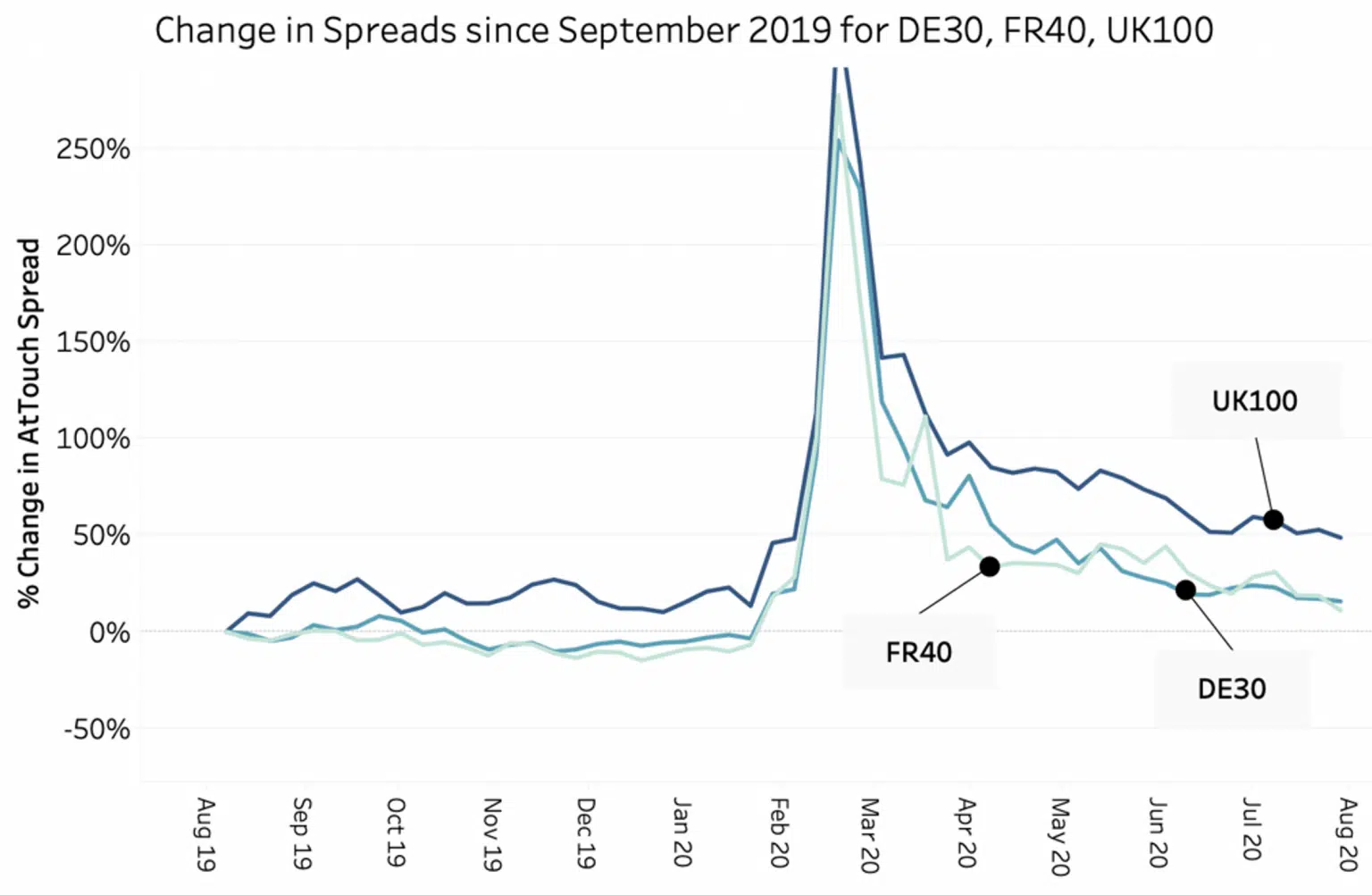

Having a good understanding of how to select a venue when executing a large trade is essential for successful performance. There are many venues to consider and each venue has its own “sweet spot”, depending on the names and size traded and that varies according to your level of urgency. Using objective criteria, such as expected time to execution and likely price impact, we can rank venues into an order of priority for routing. Furthermore, when we look at how this changes over time, we get a sense of the importance of regular monitoring and updating of the smart order routing process.

In a previous blog post, we discussed how choosing and ranking venues using liquidity or price improvement criteria depends on the trade quantity and the preference of the trader at the time of the trade. The statistical properties of three factors: the distribution of trade sizes, the number of trades per day and the price movement determine the optimal allocation between the different venues. This leads to what we call the “venue sweet spot”, a range of sizes where a particular venue will achieve its highest rank or allocation weight.

In the latest iteration of our Liquidity Intelligence tool, we introduce views that improve the understanding of venue sweet spot, detects the sweet spot and explores the evolution of the venue ranking in time. We think these views will help traders improve their understanding of the liquidity landscape and offer an optimised view of block liquidity. The attached screenshot, which is taken from the user interface, shows how the ranking changes between the top 3 venues in the EU50, for each month between January and July, in a range of sizes from €500K to €10 M. The user can see the evolution of the ranking, and react to the changing landscape. For example, for sizes between €2M and €10M, Venue A ranks number 1 from January until June, and drops to number 2 in July when Venue B takes over in the top position. Meanwhile, Venue C ranks in the number 1 position through the whole year so far for sizes below €1M. For simplicity of presentation, we took the 50 most liquid European names in dark pools, but the analysis can be performed for all available lit and dark venues and for any name and no limit to the number of venues ranked. Further detail is revealed by varying parameters for urgency and minimum acceptable quantities.

big xyt’s mission is to provide transparency to a very fragmented market. The new Liquidity Intelligence views provide an innovative way to look at the venue selection and ranking process. It brings the power of an advanced SOR to the users screen and demystifies the venue ranking problem.

At big xyt we can provide many metrics to help with fine tuning the trading process, such as daily time weighted spreads & order book depths for traders and algo developers in over 20,000 securities, and all significant venues. If you are interested in letting us do some of the heavy lifting for your algo infrastructure please get in touch

If you find these pieces of analysis useful, you will find there is a lot more you can do with our Liquidity Cockpit. Clients using our Execution Analysis/TCA are able to measure execution performance with the demonstrated precision and flexibility.

Please follow the link for more information and to see other aspects of our analysis, please follow this link

As ever we welcome feedback as this can shape further contributions from our team and to the Liquidity Cockpit tool, our unique window into European equity market structure and market quality.

We hope you enjoy them.

—

This content has been created using the Liquidity Cockpit API and other analytical tools developed for our clients.

About the Liquidity Cockpit

At big xyt we take great pride in providing solutions to the complex challenges of data analysis. Navigating in fragmented markets remains a challenge for all participants. We recognise that the investing community needs and expects continued innovation as the volume of data and related complexity continues to increase.

Our Liquidity Cockpit is now recognised as an essential independent tool for exchanges, Sell-side and increasingly Buy-side market participants. Data quality is a key component, as is a robust process for normalisation so that like-for-like comparisons and trends over time have relevance. However, our clients most value a choice of flexible delivery methods which can be via interactive dashboard or direct access to underlying data and analysis through CSV, API or other appropriate mechanism.

For existing clients – Log in to the Liquidity Cockpit.

For everyone else – Please use this link to register your interest in the Liquidity Cockpit.