Market Trends Show Significant Growth in ETF Algo Trading

The Exchange-Traded Fund (ETF) market has experienced remarkable growth, reaching an all-time high in 2024 with $3.26 trillion in turnover – a 32% year-over-year increase. As the market expands, so too does the sophistication of execution strategies available to investors. Among these strategies, algorithmic execution solutions for ETFs have gained substantial momentum over the past two years.

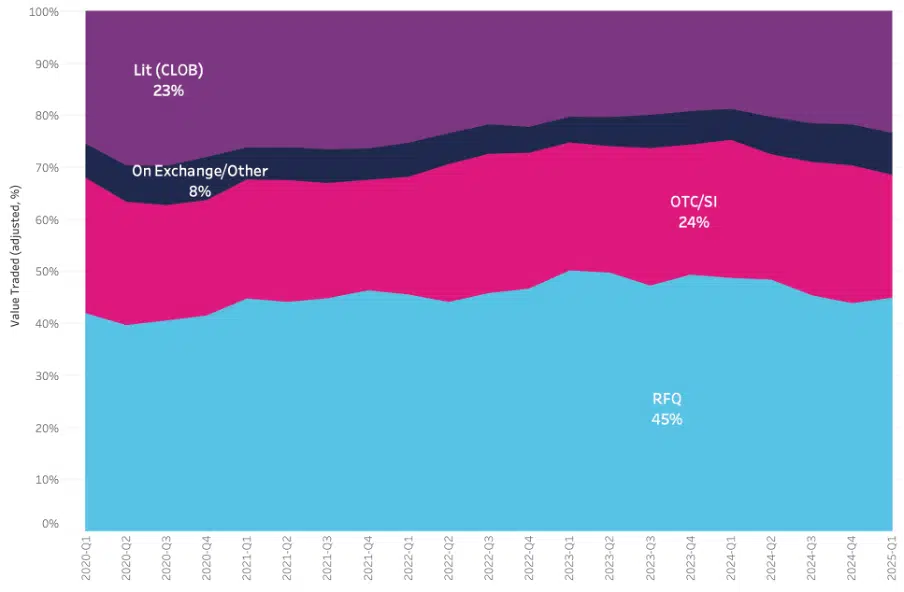

According to data from big xyt, there are changes in the market microstructure, notably lit markets are gaining traction.

ETF Trading in Europe by Mechanism

Brokers Respond with Dedicated ETF Algorithms

Various brokers have recognised the unique characteristics of ETFs and have developed dedicated algorithmic solutions to address these specificities. These specialised algorithms go beyond the capabilities of traditional cash equity algorithms, which may not be optimally designed for the nuances of ETF trading.

As BlackRock‘s Capital Markets team notes in their recent paper, “ETF Algorithm Design: Unlocking new opportunities,” ETFs have particular characteristics that differentiate them from single stocks. Using algorithms initially designed for equities might not provide the most efficient execution for ETF trades.

Insights on ETF Algorithm Benefits

The paper outlines several essential features that make ETF algorithms valuable for investors:

- Access to multiple liquidity pools – Best-in-class algorithms seek liquidity across multiple venues.

- Robust fair value integration – Effective ETF algorithms incorporate fair value concepts to determine optimal execution urgency and assess whether the ETF is trading within acceptable levels.

- Premium/discount optimisation – By tracking both current and average premium/discount levels, algorithms can adjust aggressiveness relative to market conditions.

- Tailored pre- and post-trade analysis – Enables traders to better assess execution risk and efficiency by considering both underlying market liquidity and ETF-specific metrics like premiums relative to fair value.

The paper also highlights “advanced” features, including sourcing liquidity from underlying markets and proxies, adaptive urgency scaling, clean-up logic for order completion, and live feeds providing real-time execution metrics.

The Critical Role of Pre- and Post-trade Analysis

Perhaps one of the most valuable insights is the emphasis on pre- and post-trade analysis for optimising execution outcomes – a common misconception: focusing solely on an ETF’s historical trading activity when assessing liquidity.

Instead, a more comprehensive approach that considers the ETF’s underlying basket and futures market makes sense. By combining these volume profiles, dealing desks can better evaluate potential market impact from algorithmic orders.

For post-trade analysis, examining not just standard Transaction Cost Analysis (TCA) metrics but also ETF-specific metrics such as arrival premium, execution premium and premium reversal.

How Can big xyt Help?

big xyt is referenced by the industry as a trusted source of liquidity statistics for secondary markets and offers the buy and sell-side essential historical and real-time data on ETF liquidity and EBBO benchmark prices, crucial for effective pre- and post-trade analysis, as well as other services including TCA. Investors, issuers, exchanges and market makers all rely on our comprehensive market analytics to make informed decisions.

As ETF algorithmic execution continues to evolve, having access to accurate, independent data becomes increasingly crucial for all market participants looking to optimise their trading strategies and improve execution outcomes.

Conclusion

The ETF execution landscape is evolving, offering investors new tools and approaches to navigate the market more effectively. As execution strategies continue to develop, investors should stay informed about the latest advancements and leverage the best available resources to optimise their trading decisions.