Day 8 of 12: Total vs Adjusted Volumes Traded

How non-addressable SI volumes can mislead liquidity expectations.

Understanding where the expected liquidity is available is key to any participation strategy. However, if your assumptions relating to expected liquidity include all reported trades, you could find yourself starting from the wrong place.

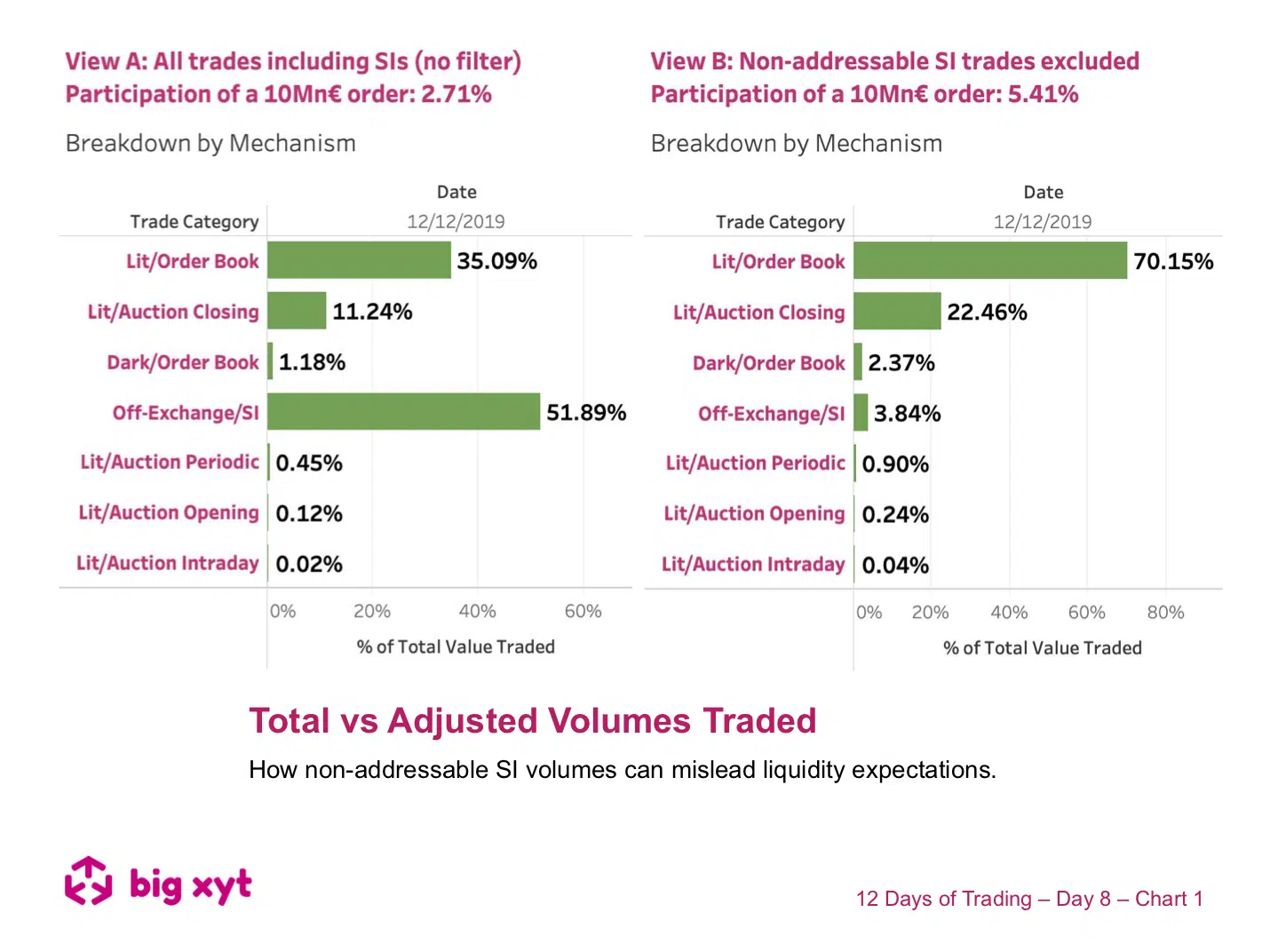

This example looks at Munich Re shares traded on the 12th December (a relatively “normal” day before the UK General Election results were announced). A typical institutional sized order of €10Mn would need to be careful not to impact the market.

In view A, on the left, the order represents 2.71% of the days total reported turnover in the stock. But how much of the Systematic Internaliser (SI) volume is unaddressable and gives an over optimistic picture of available liquidity?

In view B we have adjusted the SI volume by filtering out the non price forming & unaddressable trades (please contact us if you are curious about the methodology we apply). The resulting picture changes noticeably as the order now represents 5.41% of adjusted traded volume and target participation in all available venues & mechanisms would need to be doubled to fully execute the order in one day.

Liquidity Cockpit users are able to look at any stock this way and see the venues broken down. Clients using our Execution Analysis/TCA are able to measure execution performance with the demonstrated precision and flexibility.

We’re delighted to share that big xyt has been shortlisted for, not one, but two industry awards!

We have made the shortlist for ‘Best Trading Analytics Platform’ and ‘Transaction Cost Analysis (TCA) Tool for Best Execution’ at the TradingTech Insight Awards 2020. We’d really appreciate your support in gaining recognition for our work in the industry.

Please spare a few moments to vote for us here. Thank you in advance.

—

Do you want to receive future updates directly via email? Use the following form to subscribe.

On our 12 Days of Trading

As the year draws to a close we have been asked by clients to repeat our festive exercise on the 12 days leading up to the holidays. As a result, you will find a post to a different 2019 big-xyt observation each day. We look and highlight trends since the introduction of MiFID II with a focus on this year’s changes or events.

We hope you enjoy them.

—

This content has been created using the Liquidity Cockpit API.

About the Liquidity Cockpit

At big-xyt we take great pride in providing solutions to the complex challenges of data analysis. Navigating in fragmented markets remains a challenge for all participants. We recognise that the investing community needs and expects continued innovation as the volume of data and related complexity continues to increase.

Our Liquidity Cockpit is now recognised as an essential independent tool for exchanges, Sell-side and increasingly Buy-side market participants. Data quality is a key component, as is a robust process for normalisation so that like-for-like comparisons and trends over time have relevance. However, our clients most value a choice of flexible delivery methods which can be via interactive dashboard or direct access to underlying data and analysis through CSV, API or other appropriate mechanism.

For existing clients – Log in to the Liquidity Cockpit.

For everyone else – Please use this link to register your interest in the Liquidity Cockpit.